With last week’s strong economic stats and inflation basically flatlined, many believe there will be a soft landing and no recession. However, there are stats saying that, with the yield curve so inverted (most since 1983), recession can and probably will still happen.

Recession can take time to emerge, with expectations that it won’t occur until 2024 or 2025. First though, we still see stagflation.

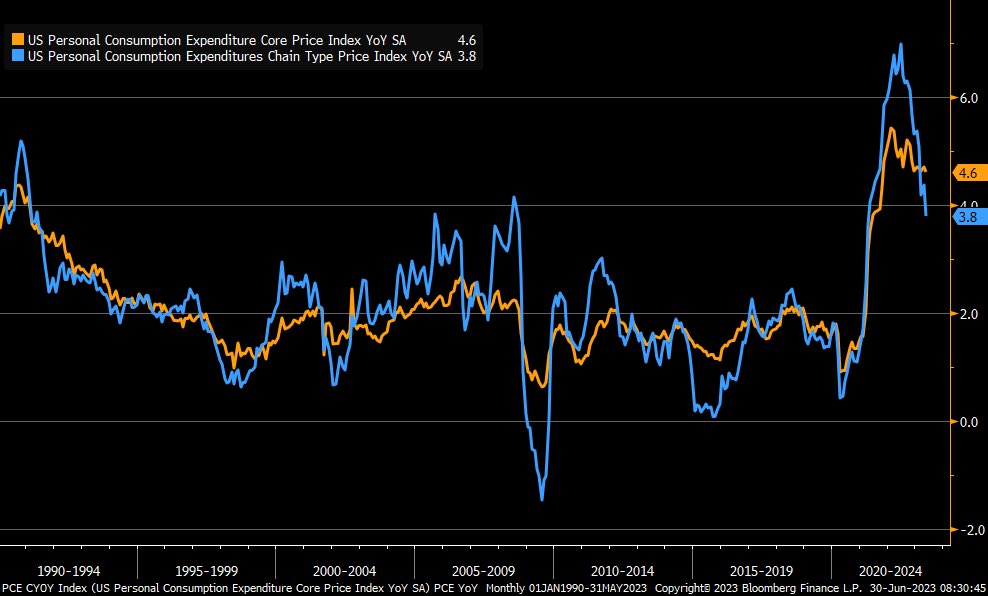

5.4% core CPI in Europe and 4.6% PCE U.S. are just the numbers we need to infer that banks could still raise rates, but the speed (for sure) and perhaps the number of times they raise is coming to an end. The FED wants a weaker jobs market, and we could see that in the near-future. Plus, a new round of inflation. Regardless, the market anticipated a bull run for the first 6 months of the year, as it is forward thinking.

The market saw the rate of change for interest rate hikes slowing, the economy most likely not contracting further, inflation potentially peaking, and the technology sector cheap and appealing. We can certainly thank the consumers in large part for the great economic stats as they are the reason the market and economy have been stronger. YOLO?

If we had to define current sentiment into two categories, it appears anger (France) and fatalism (YOLO) win. However, now that GDP rose for 3 quarters consecutively, one must wonder whether the market will continue to project further economic strength for the second 1/2 of the year.

In the case of small caps, a trading range prevails, which means we need to see small caps show new leadership to remain bullish. We also need to see other consumer areas surface, besides the large rallies thus far in airlines and cruise ships. On the monthly chart, IWM has yet to demonstrate any real expansion.

On the Daily chart, the middle chart or our Leadership Indicator has IWM underperforming the S&P 500 benchmark. The Real Motion or momentum indicator at the bottom illustrates a bullish divergence. Hence, IWM must get moving in price for a more roseate second-½-of-the-year setup.

Now, add in the uncertainties around the world such as weather (drought and floods), Russia (is it over?), China (more chip wars), global inflation (still sticky), supply chain (de-globalization), labor (wages rising), and social unrest (France), and the one-way call for disinflation seems way too one-way. Flexible and active traders will prevail for the next 6 months.

Other than some volatility in the commodities area along with the recent healthy correction, we still maintain a stagflation environment will persist until 2025.

Looking at the 30-year cycles in commodities versus stocks (going back to 1933), the next 15 years starting this week, are projected to see commodities outperforming by potentially more than 3:1.

We are watching the 20+ year long bonds (TLT) for clues. So far, the bonds have not moved much. A rally from current levels (over 104) and we will become more defensive in equities. And, most likely, more friendly to commodities and precious metals.

Finally, we have eyes on the U.S. Dollar versus the Euro. The dollar stopped right at the resistance level of .92. Under .90, we would expect more dollar weakness.

Last week’s daily’s were filled with trading ideas including in the oil, energy, materials, and transportation sectors. Don’t miss a Market Beat-sign up for the free updates now!

Mish in the Media

Mish runs through bonds, modern family, commodities ahead of PCE on Benzinga.

Mish explains her bullish call on Bitcoin and provides her price target for the cryptocurrency in this video appearance on CNBC Asia.

Mish shares why the transportation ETF is such an important measure of economic strength and how retail stocks (XRT) continue to underwhelm on the Tuesday, June 27 edition of StockCharts TV’s The Final Bar with David Keller.

Mish discusses how business have been watching Russia in this appearance on Business First AM.

Read Mish’s commentary on how the situation in Russia impacts the markets in this article from Kitco.

Watch Mish’s 45-minute coaching session for MarketGauge’s comprehensive product for discretionary traders, the Complete Trader.

On the Friday, June 23 edition of StockCharts TV’s Your Daily Five, Mish covers a variety of stocks and ETFs, with eyes on the retail sector for best clues in market direction.

Read Mish’s interview with CMC Markets for “Tricks of the Trade: Interviews with World-Class Traders” here!

Mish delves into the potential next market moves for several key markets, including USD/JPY, Gold and West Texas crude oil in this appearance on CMC Markets.

Mish and Dale Pinkert cover the macro, the geopolitical backdrop, commodities, and stocks to watch on FACE Live Market Analysis and Interviews.

Mish and Ashley discuss buying raw materials and keeping an eye on Biotech on Fox Business’s Making Money with Charles Payne.

Coming Up:

June 29: Twitter Spaces with Wolf Financial (12pm ET) & CNBC Asia (9pm ET)

June 30: Benzinga Pre-Market Prep

July 6: Yahoo Finance

July 7: TD Ameritrade

ETF Summary

S&P 500 (SPY): Needs one more push or begins to look a bit toppy based on lethargic momentum.Russell 2000 (IWM): 190-193 still the overhead resistance to clear.Dow (DIA): 33,500 major support to hold.Nasdaq (QQQ): Still working off a reversal top until it takes out 372.85.Regional banks (KRE): Need a new move over 42.Semiconductors (SMH): 150 support.Transportation (IYT): 250 resistance and a potential correction/mean reversion in store.Biotechnology (IBB): 121-135 range.Retail (XRT): 63 support.

Mish Schneider

MarketGauge.com

Director of Trading Research and Education